In this final instalment of our 3-part series, we look at bioscience platform companies as they mature into focused product businesses. What drives this transition? What are the key success factors as a focused product business? This article covers in more detail Stage 4 of the lifecycle of bioscience platform companies depicted below:

The complete 3-part series can be downloaded here as a single pdf document

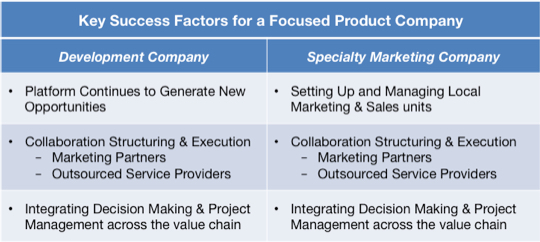

Stage 4 – Focused Product Company

As the company progresses, one or two of its projects start to exhibit a high probability of reaching the market in the not-too-distant future. Often these are proprietary projects, but they could also be technology/service provision collaborations with substantial future royalty streams. Since the company by this stage is typically already listed on the capital markets, investment analysts begin ascribing the majority of its valuation to these “lead” projects. This in turn drives the company’s owners and management team to focus their efforts on the lead projects, investing in new capabilities to ensure their success and if necessary, diverting resources from the other projects when funds are short. Such focus makes it easier to raise new funding from the capital markets to support the investment, creating a virtuous circle that drives the transition to a product company focused in a particular application area. This pressure to become a product company is inevitable once the lead projects attain high visibility – the investor community finds it difficult to value a company with small pieces of the pie in many disparate application areas.

“We have a lot of investors who say of our broad portfolio of programs, ‘It’s too much, I can’t get my head around it. My methodology is to look at single compounds, take a deep dive, analyze the market, the competition, and I can put a value on that asset. But 10, 20 or even more assets, I’m not even going to start, it’s too much work’.”

“Analysts will only focus on one or two of the programs, so they disproportionately skew the company in terms of its valuation around these one or two programs. That’s a real challenge for a platform company. You haven’t got a label. What are you? Are you an oncology company? Are you a diabetes company? What are you?”

Notwithstanding the pressure to become a focused product company, there are several variants to how this business model can be realized:

- Development Company which develops and registers a portfolio of products within one or two specific therapeutic areas, for marketing through global distribution and selling partners.

- Specialty Marketing Company which markets high margin niche products in one or two specific therapeutic areas with its own salesforce across a selected set of geographic markets.

- Combination of (1) and (2).

Being a Development Company makes sense if the company’s platform continues to generate new opportunities, especially if the targeted therapeutic areas are “mass market” ones with lots of prescribers e.g. diabetes or asthma. In this variant of the focused product company model, the critical success factors revolve around integrating decision making and project management in the later stages of the value chain such as clinical development, technical product development, manufacturing scale-up, regulatory strategy, physician positioning and pricing/reimbursement strategy. Since it will not make economic sense to maintain a full suite of in-house operations all of these areas, the company will typically leverage outsourced service providers in many of them e.g. clinical trial monitoring. At the same time, the company will need to contract and work with one or more marketing partners globally for each product. Typically these will be funded co-development arrangements initiated after Phase 2 clinical studies in those cases where the cost of taking the product to regulatory approval is excessive for it to bear alone. The ability to structure and execute collaborations thus continues to be a critical success factor, with marketing partners as well as outsourced service providers.

“Over the last five years, of those companies that have brought their first cancer product to market, those that have co-commercialized have very clearly been the most successful. Those that have tried to do it on their own, or who have given it all away, have done the worst.”

Being a Specialty Marketing Company makes sense if the targeted therapeutic areas are of a specialist nature that require a comparatively small sales force e.g. oncology or an orphan disease, especially if the company’s platform is becoming commoditized and is less likely to continue reliably generating a slew of unique new opportunities. In this variant of the focused product company model, the same capabilities in decision making and project management integration across development and strategic marketing mentioned above will again be a critical success factor. Furthermore, the ability to set up and manage local marketing and sales units will also be essential to success. A typical approach when initiating this strategy is to in-license or acquire a portfolio of products already on the market in the target therapeutic areas so as to build up prescriber and payer relationships and capture market insights in anticipation of the lead projects in the pipeline. In this case, the sales and marketing capabilities need to be built very early on. Nevertheless, since the company is unlikely to have a local presence in every market, marketing partners will still be required in certain geographies. Collaboration structuring and execution will thus continue to be important for these marketing partners as well as for outsourced service providers.

“Adding Marketing & Sales creates completely different classes of problems to overcome, as well as a major enforced culture change. It’s a much bigger management shift than sticking with managing technical/scientific issues.”

A Combination of Development and Specialty Marketing is not impossible of course, and some companies do seem to go down this route. But the underlying cultures and business values of the two variants are quite different, with the former being very product/platform-oriented and the latter being very physician/market-oriented. Hence this approach is probably difficult to carry off without one variant being the major driving force. For example, it can make sense to be primarily a development company, with a salesforce in say one or two large markets (or perhaps just in the home market) as a way of capturing market intelligence and increasing profitability without taking on undue risk or diluting the company’s culture. Conversely, one could be primarily a specialty marketing company with a focused development arm to exploit know-how and increase company valuation.

An important point to note is that there will be companies successfully operating the above business models who did not arrive there from a platform history. The newly-transitioned platform company will be judged against a different set of benchmarks i.e. other focused product companies – not just by investors and prospective collaborators, but also by regulators, payers, physicians and patient lobbying groups.

Forever Platform?

One question that is often asked is whether the company could remain a technology provider or hybrid company forever, instead of taking on the cost and risk of adding new capabilities and in essence gambling on the success of the lead projects. An oft-quoted example is that of ARM Holdings plc (“ARM”), the dominant global player in mobile technology for smartphones and tablets. ARM focuses on creating and licensing intellectual property – its chip designs are used in almost every mobile phone and tablet but it does not manufacture any of them itself and neither does it have an end-user sales force. Nevertheless, it has a market capitalization of nearly US$ 20 billion with an operating income in excess of 20% of sales. However one key difference is that the application market for ARM is very specific and clearly defined whereas a bioscience platform company with 10 to 20 separate projects for applications in say diabetes, alzheimer’s, pain, arthritis, asthma and cancer is much harder for the investor community to get their arms around since the underlying demand drivers are very different. And so the valuation focus always narrows in on the lead projects closest to market.

To overcome this valuation challenge, one possibility might be to create spin-off entities for each project (or group of closely-related projects) once a certain stage in development in reached, with separate investors for each entity according to their preferences for the different end-user markets, risks, returns and timelines. Each such project-centric entity would initially operate a virtual model, contracting in the relevant management and technical capabilities from the “mother” company. Over time, the successful project-centric entities would evolve into listed focused product companies of their own or be acquired by trade buyers. While the mother company would continue to use its platform to generate and nurture new opportunities in a diverse range of areas.

“If someone says to me I love that asset, I want to see it in a separate vehicle, I want to put in tens of millions to give it a chance of working, ultimately that model stands a better chance of success because they will always look at that asset differently as a separate entity than an asset within a hybrid organization.”

“A possibility might be single asset joint venture spinout, take it out, fund it elsewhere, we put in half the stake, the rest from outside, but effectively it’s still our drug.”

Concluding Remarks

Platform companies are a critical component of the bioscience ecosystem. They can add tremendous value across a range of therapeutic areas. And they provide both the critical mass of know-how, and the incubation time, for certain innovative technologies to be fully developed and exploited. Not everything being spun out of academia or an existing business is best exploited via the virtual project-centric model that many venture capital firms seem to be favoring these days. And in any case, value can often be maximized via a diversity of applications rather than focusing too early on just one.

Platform companies are also a good base to spawn new sustainable product companies who can deliver increased innovation and improved outcomes across the healthcare system. The market pull for the successful platform companies to evolve into focused product companies is almost inevitable despite the management challenges involved. Nevertheless, there may be some creative mechanisms for having the best of both worlds, by spinning off single asset entities for commercialization and marketing, while retaining the platform core in the original mother company.

The complete 3-part series can be downloaded here as a single pdf document

Author’s Note: The content in this series of articles synthesizes (i) my own experiences working with bioscience platform companies, and (ii) perspectives volunteered by the leaders of such companies. For example, the quotations which appear in this series of articles emerged from an informal workshop I chaired in the summer of 2014 with the leaders of four drug discovery platform companies. Since the meeting took place in a pre-competitive setting under the Chatham House Rule, neither the individuals, their companies nor the quotation attributions can be identified. Nevertheless, all assertions and opinions in this series of articles are mine alone and do not necessarily reflect the views of the four individuals nor their companies.