What are bioscience platform companies? And how do they eventually develop into fully-fledged product businesses? Most industry participants, commentators and investors recognize and understand start-up biotech companies at one extreme, and fully-fledged pharmaceutical and medical device product companies at the other. However bioscience platform companies are neither. They can be very healthy businesses, yet bereft of product revenues or even profits for many years. And for much of their lifecycle, they can be very difficult for investors to pin a precise valuation on.

In this initial instalment of a 3-part series , we will first define what the term “bioscience platform company” encompasses. We will then outline the key evolutionary stages of such a company. Subsequently, in our second instalment, we will look at its adolescent and early adulthood stages, considering the principal drivers for transition to these stages and the key success factors during these stages. And in our final instalment, we will look at this type of company as it matures into a focused product business. Our aim with this series of articles is to help the management teams and investors of bioscience platform companies to more effectively navigate their strategic journey.

The complete 3-part series can be downloaded here as a single pdf document

What is a Bioscience Platform Company?

The phrase “bioscience platform company” typically refers to an enterprise whose business model includes three important aspects:

- The company is built around certain comparatively scarce scientific core competencies.

- These compentencies are deployed to enable the generation of a succession of new therapeutic or diagnostic product candidates.

- Application of these compentencies is spread across a wide range of therapeutic areas and specific indications.

While such a company is often centered around a branded proprietary technology (hence the phrase “platform technology company”), there are also platform businesses based just on unique know-how, for example, companies skilled in therapeutic peptides, fragment-based drug discovery or protein engineering. In this latter situation, the companies usually do not brand their platform and many do not even see themselves as having a “platform” per se. Branded or otherwise, both sub-types exhibit similar business characteristics and are included in the scope of this article. What we do not include under this definition is the “classic” biotech/medtech start-up focused on a single very high potential application. Nor do we include here those companies providing contract services which are essentially commoditized.

Today, our state of knowledge in biotechnology and how diseases can be diagnosed and treated is comparatively far behind that of for example information technology or aerospace technology. Platform companies provide the critical mass of people, time, funding and application breadth for new untested bioscience technologies to develop and be eventually applied against the widest range of potential healthcare applications. This is something which arguably neither large established pharmaceutical and medical device corporations, nor start-up biotech companies, are best set up to handle.

For consistency of narration, this series of articles adopts a drug discovery flavor. Nevertheless, everything here applies to other stages in the new drug life cycle, as well as to devices and diagnostics, for example inhaler devices, bio-materials, modified release dose formulation, and so forth.

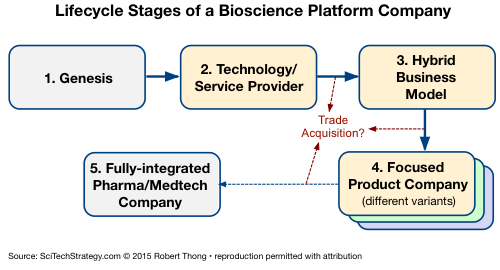

Key Stages in the Lifecycle of a Bioscience Platform Company

A bioscience platform company evolves through several key stages:

The company typically has its genesis as an academic start-up or a spin-off from an existing pharmaceutical or medical device business. It could have been conceived from day one as a platform company. Or it could have started life as a “classic” biotech seeking to take a single product idea to market, only for that original idea to run aground or for the company to run out of cash. In either case, the company needs to generate revenue by providing its platform to other companies.

If it can generate revenue consistently, it will establish itself as a credible technology and/or service provider i.e. Stage 2 in the diagram above. At this stage, it is still very much an awkward adolescent, trying to find its way in the world where others seem to hold all the cards. Its business comprises multiple technology and/or service provision contracts with a portfolio of customers who use the platform for their own projects and products. Licensing (if the platform involves proprietary technology) and contract R&D work is the usual business arrangement. There may be a risk-reward sharing element in these arrangements e.g. milestone payments and small single digit royalties on future sales. But nevertheless their customers are the ones who own, fund and control the direction of the projects.

At Stage 3, the company moves into young adulthood. It starts to originate, fund and direct proprietary projects of its own until they are much closer to the market. While in most cases, these proprietary projects will still eventually be partnered with commercial collaborators at a much later stage, at this point, the company makes the decisions, bears the risks and captures the rewards.

Since the company now requires even more cash flow for funding its proprietary projects, it will continue or even expand its portfolio of technology/service provision deals. Hence it operates a hybrid business model, continuing the type of business arrangements which were the staple of the previous stage while simultaneously pursuing its own proprietary projects.

Eventually, the company reaches maturity at Stage 4, when its proprietary projects begin to dominate management attention and enterprise man-hours. As a focused product company, its valuation by investors is now founded on anticipated revenues from one or more specific commercial products which are close to (or already on) the market. Operationally, the company continues to concentrate in-house on certain key activities, relying on outsourced service providers and collaborators for other aspects of its value chain. As we will see later in this series of articles, there are a few variants to how this business model can be realized at this stage.

During the second, third or fourth stages, there is always the possibility of the company being acquired by a customer, collaborator or competitor – the probability increasing rapidly as it evolves through stages three and four in particular. Acquisition could happen for both positive or negative reasons. In the former case, one or more of the projects develops huge commercial value and becomes strategically essential for another player to control. In the latter case, the failure of certain projects leads to a loss of investor confidence, enabling an opportunistic acquirer to buy the company and gain control of its platform.

If the company is not acquired by a trade buyer, its original owners will typically engineer a stock market listing via an Initial Public Offering (“IPO”) sometime during the second or third stage, depending on the attractiveness of both the capital markets and its customer and project portfolio at the time.

In a few cases, the company may make it all the way to Stage 5 and become a fully-integrated pharmaceutical or medical technology company, conducting the bulk of its manufacturing, marketing and sales in-house, in addition to continuing the R&D activities which were its roots. Having said that, many companies and their investors find it makes sense to remain as focused product companies i.e. sustained growth in its valuation is not tied to having a complete in-house value chain.

Coming Up Next

In our next instalment of this series, we will look in more detail at the adolescent and early adulthood stages of bioscience platform companies, considering the principal drivers for transition to these stages, and the key success factors during these stages.

The complete 3-part series can be downloaded here as a single pdf document

Author’s Note: The content in this series of articles synthesizes (i) my own experiences working with bioscience platform companies, and (ii) perspectives volunteered by the leaders of such companies. For example, the quotations which appear in this series of articles emerged from an informal workshop I chaired in the summer of 2014 with the leaders of four drug discovery platform companies. Since the meeting took place in a pre-competitive setting under the Chatham House Rule, neither the individuals, their companies nor the quotation attributions can be identified. Nevertheless, all assertions and opinions in this series of articles are mine alone and do not necessarily reflect the views of the four individuals nor their companies.